India’s Road Recycling Machine

How a little-known financial instrument is turning old highways into new ones

Here’s a fact that might surprise you: India has the world’s largest road network - over 6.6 million kilometres of it. The government has poured money into building highways at a pace few countries have matched, scaling public infrastructure capital outlay from ₹2.5 lakh crore in FY14 to ₹12.2 lakh crore in the FY27 budget estimate. That’s a jump from 1.7% of GDP to 3.3%.

But here’s the thing: building roads is only half the problem. The other half is figuring out how to pay for the next batch without drowning in debt. And that’s where a financial instrument most people have never heard of - the Infrastructure Investment Trust, or InvIT is helping India finance its highways.

What’s an InvIT, really?

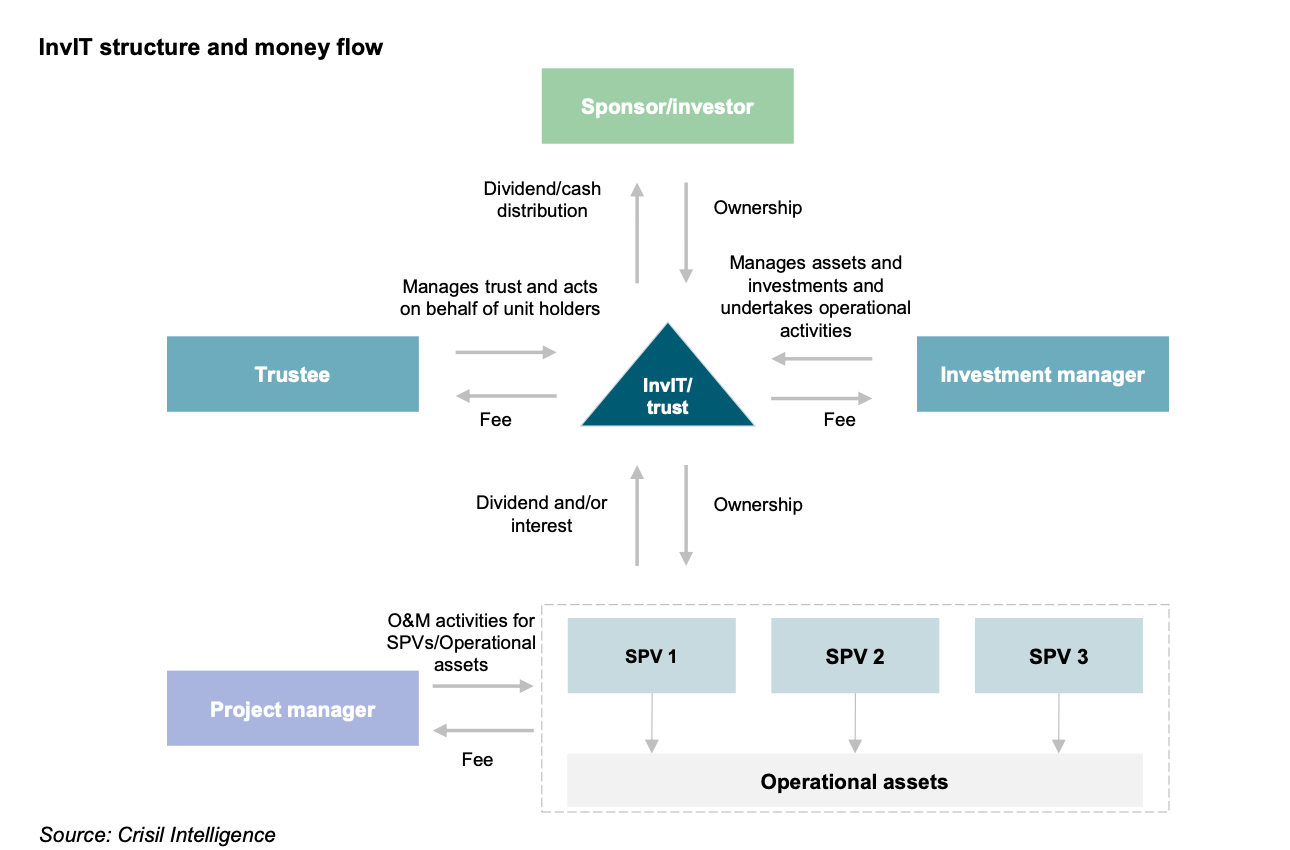

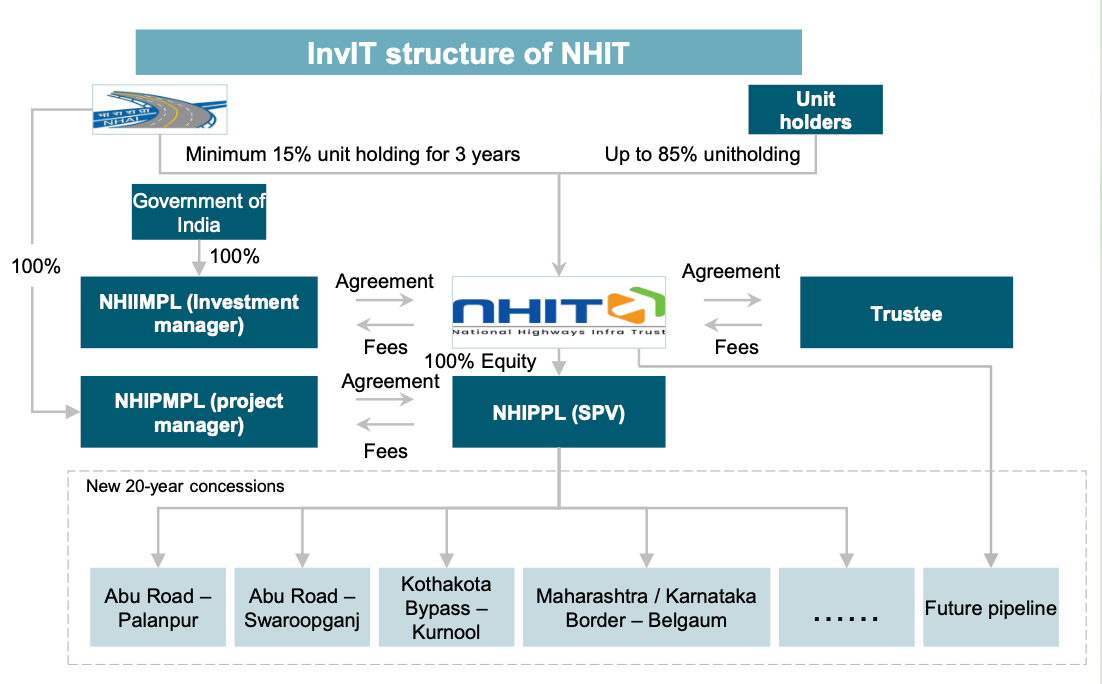

Think of an InvIT as a mutual fund, but instead of holding stocks or bonds, it holds toll roads, highway stretches, and other income-generating infrastructure assets. A sponsor, say, NHAI or a private road developer transfers operational road assets into a trust. The trust issues units to investors. Toll revenues and annuity payments flow through the trust to unit holders as regular distributions.

The sponsor gets upfront capital. Investors get a steady yield. And the road stays publicly owned, this isn’t privatisation. Ownership doesn’t change hands. Only the right to operate and collect revenue transfers for a fixed concession period, typically 15 to 30 years

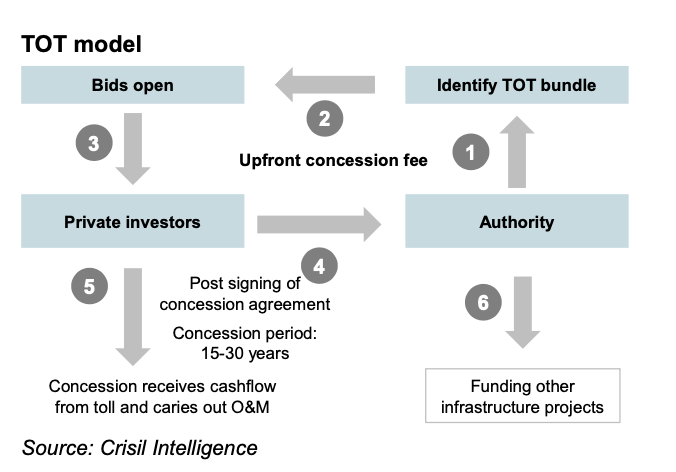

Now, this matters because InvITs solve a problem that India’s older monetisation tools couldn’t. Before InvITs, the government’s primary instrument for recycling capital from existing roads was the Toll-Operate-Transfer (TOT) model - essentially a one-shot auction where a private bidder pays a lump sum upfront for the right to toll a highway bundle. TOT worked. NHAI awarded 10 bundles covering 2,689 km and raised about ₹49,000 crore between FY19 and FY25.

But TOT is a one-time transaction. Once you sell the concession, the capital recycling stops. There’s no mechanism for adding more assets, no platform for ongoing portfolio management, no secondary market for investors to trade in and out. InvITs, by contrast, are platforms. Assets can be injected over time. Units can be listed and traded. New investors can enter through follow-on offerings. It’s the difference between selling your house and renting out rooms while keeping the deed.

From a trickle to a flood

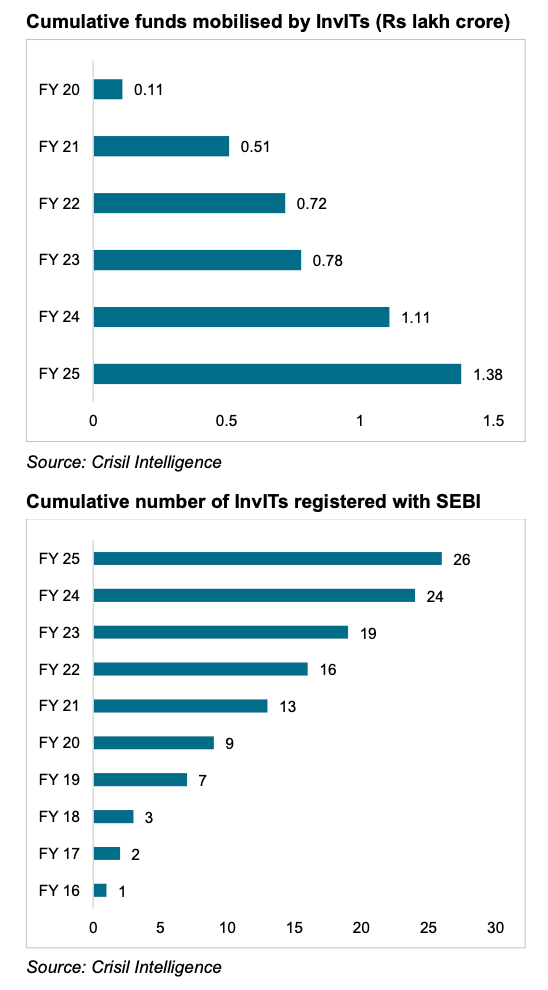

India’s first InvIT, the IRB InvIT Fund listed in 2017, raising about ₹4,745 crore. Early investors included the Government of Singapore and Deutsche Global Infrastructure Fund. It was an experiment. Could toll road cash flows really attract institutional capital through a trust structure?

The answer, evidently, was yes. By FY25, 26 InvITs had registered with SEBI, of which 15 were road-focused. Cumulative funds mobilised surged from ₹0.11 lakh crore in FY20 to ₹1.38 lakh crore in FY25 - a compound annual growth rate of roughly 65%. Road InvIT assets under management alone hit ₹2.46 lakh crore, growing at a 42% CAGR over the same period. Roads now account for 39% of total InvIT AUM, up from 18.5% in FY21.

The government’s own vehicle, the National Highways Infra Trust (NHIT), set up by NHAI in 2020 completed four monetisation rounds by FY25, transferring 26 highway projects spanning 2,345 km and raising over ₹44,000 crore. Its investor roster reads like a who’s who of global patient capital: the Canada Pension Plan Investment Board, Ontario Teachers’ Pension Plan, and Singapore’s GIC, among others.

See, this is the part that often gets missed in policy discussions about infrastructure financing.

The constraint isn’t just how much money India can spend on roads. It’s how fast capital locked in existing highways can be freed up and recycled into new ones.

NHAI facilitated ₹72,000 crore of debt repayment between FY23 and FY25, backed by ₹1.4 lakh crore monetised since 2020. That’s not new borrowing. That’s the same capital going around twice.

The penetration gap

And yet, for all this growth, the penetration remains startlingly low. As of FY25, only about 15,700 km of tollable, revenue-generating road assets sat inside InvIT structures, out of roughly 325,000 km of national and state highways. That’s a penetration rate of 4.8%.

The government clearly sees the runway. Under NMP 2.0, launched in February 2026, the highway monetisation target is ₹4.14 lakh crore over FY26–30, with ₹3.35 lakh crore planned through InvITs and TOT alone, covering an additional 19,200 km. Crisil Intelligence projects road InvIT AUM could reach ₹5.45 lakh crore by FY30, more than doubling from today’s levels.

The investor mix is also evolving. Sovereign wealth funds, pension funds, and insurance companies have anchored the institutional side.

But retail participation remains thin - limited awareness, perceived complexity, and the fact that most road InvITs are privately listed rather than publicly traded.

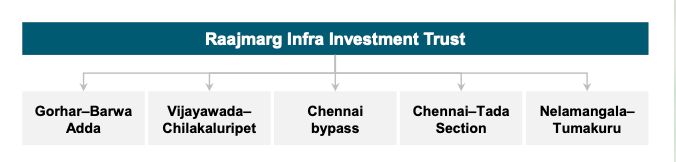

NHAI’s upcoming Raajmarg Infra Investment Trust (RIIT) - the first government-backed InvIT open to public and retail subscription, rated AAA by CARE could change that equation. It holds five toll projects across Tamil Nadu, Karnataka, Andhra Pradesh, and Jharkhand, with an average tolling history of over 15 years.

Beyond the balance sheet

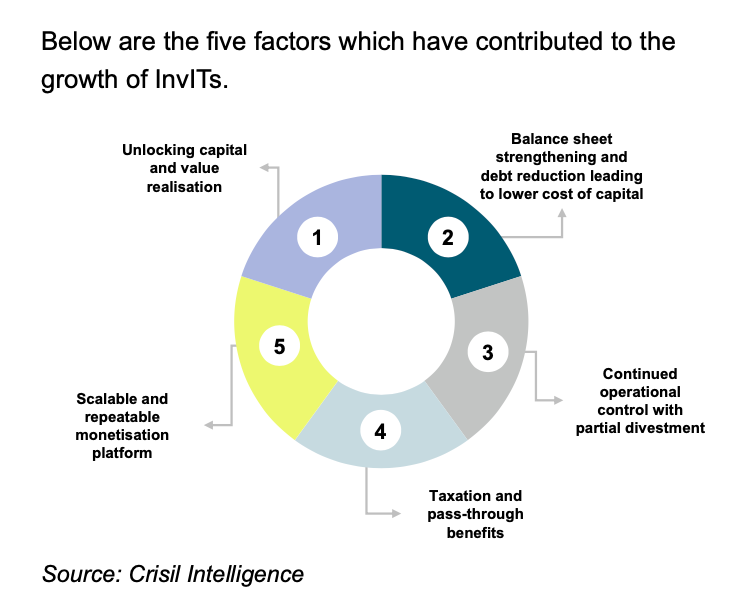

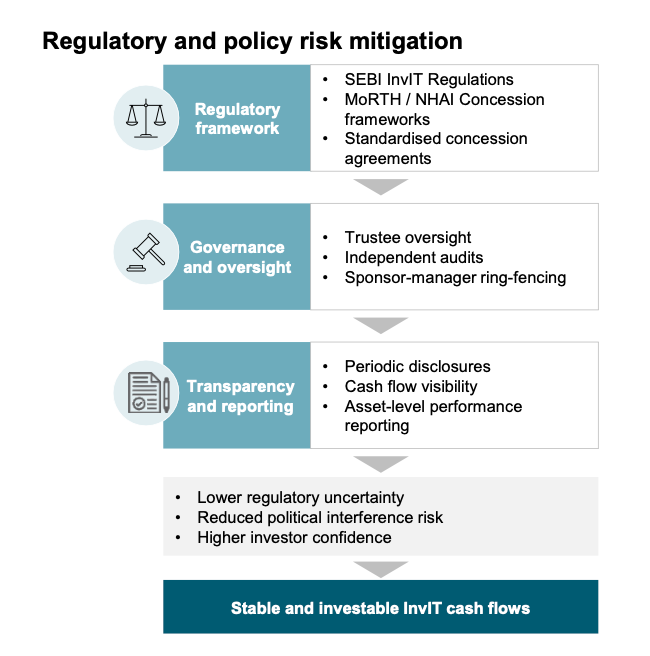

What makes InvITs genuinely interesting isn’t just the financial engineering. It’s what happens after the assets enter the trust. Because InvITs are regulated platforms with mandatory disclosures, professional investment managers, and distribution obligations, they impose a discipline on road asset management that standalone concessions rarely do.

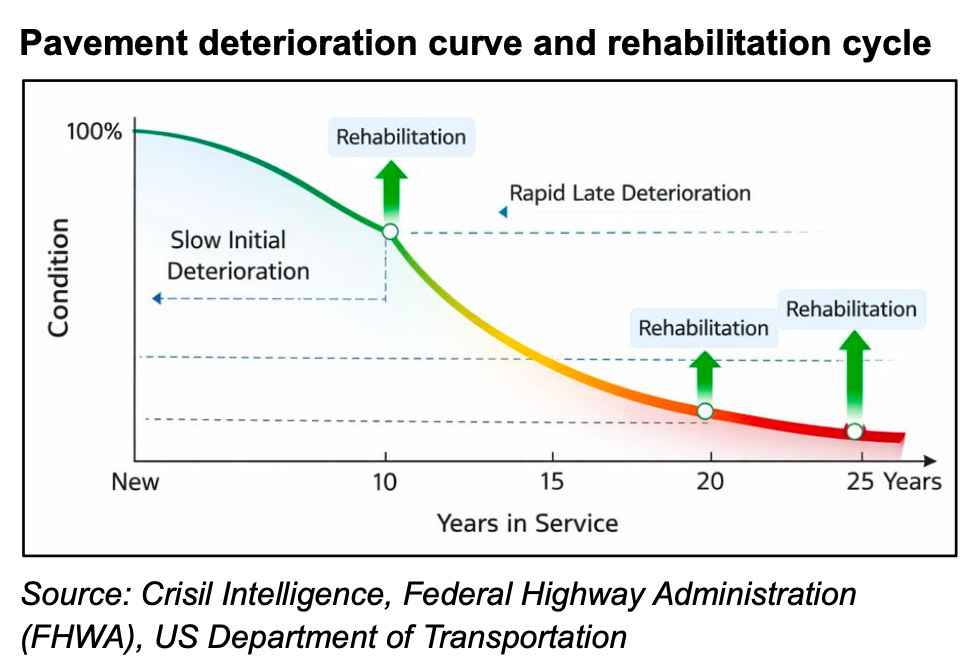

The FICCI-Crisil report highlights how leading InvITs are adopting lifecycle costing, evaluating total maintenance expenditure over an asset’s full service life rather than minimising year-to-year costs. NHAI’s Drone Analytics Monitoring System (DAMS), operational since October 2024, uses AI-enabled drone surveys across 53,000+ km in 24 states to detect pavement distress before it escalates.

The US Federal Highway Administration estimates that every dollar spent on preventive maintenance saves $6 to $10 in avoided rehabilitation costs. For InvITs holding assets over 20-year horizons, that arithmetic is transformative.

The deeper question, though, is whether India can convert this financial innovation into a genuine infrastructure flywheel, where monetisation proceeds fund new construction, which matures into new monetisable assets, which attract fresh capital, and so on. The plumbing is now in place. The capital is willing. Whether the pace of new road awards and project execution can keep feeding the machine is what will determine if road InvITs remain a clever financing trick or become the backbone of India’s infrastructure story for the next decade.